How Self-Funding Works:

A Guide to Modern Group Health Benefits

Self-Funding 101

Self-funded health benefit plans give employers and their employees added protection against spiraling health care costs, especially in light of the Patient Protection and Affordable Care Act (PPACA).

Unlike the traditional health benefits plan model, costs are controlled by the employer -- not an insurance company. Employers set the level of benefits they wish to offer and the cost for employers each year.

Costs of self-funded plans are similar to an insurance premium and include administration fees and all medial claims costs, as well as stop-loss premium payments. Stop-loss insurance limits a company's exposure on medical costs to a set level.

Employees are charged a set monthly fee, established by the employer sponsoring the health plan benefits. The employer pays the medical claims costs incurred by the covered persons enrolled in the plan. These costs are different each month, depending on the cost of care paid for covered persons. If claims costs exceed the catastrophic claims level established for the policy, then stop-loss insurance reimbursements are made to the employer.

If medical costs do not reach the annual amount budgeted, then the employer can collect a refund on the unused medical costs. Historically, about half of companies obtain refunds.

Start your Group Risk Assessment today and find out if a self-funded plan can work for your company.

Defining the Difference: Fully Insured vs. Self-Funded

Today's health care system is riddled with complex plan designs and rigorous government regulations. States have not standardized their regulations to one sensible approach. However, in recent years Federal regulations have come to provide higher levels of consumer protection than ever before.

For an employer (or Plan Sponsor) to understand the difference between "fully insured" health plans and self-funded health plans, it is easier to first discuss the typical buying arrangement:

Fully Insured

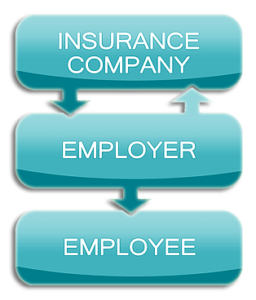

An employer, or plan sponsor, simply facilitates the purchase of a group contract that insures each of his employees directly. In essence, the insurance certificate contains an insuring clause or a promise to pay benefits. The insurance carrier makes this promise to each employee. The Plan Sponsor simply facilitates the purchase of the group contract for purposes of benefit selection, rate guarantees, and premium collection.

Self-Funded

These plans work a little differently. The employer, or Plan Sponsor, makes the promise to pay benefits to each employee, and then purchases administrative services (handling the money and the paperwork) and stop-loss insurance to protect the Plan from unexpected financial obligations of that promise.

Among the benefits of self-funding, the following elements highlight potential advantages that cannot be ignored:

- Composite Rates - Simplify Defined Contribution

- No PPACA Rebate Reporting - Keep the Claims Savings in the Plan

- Standard Benefits Across State Lines - No need for multiple plans across state lines

- Rates You Deserve - Earn better rates for deserving groups

Flexibility in Self-Funded Plans

Employers can employ great flexibility to meet employer and employee needs when creating their health benefit plans with self-funded insurance.

Often, consumer-directed health plans such as a Health Savings Account (HSA) or Health Reimbursement Account (HRA) can be incorporated into the health benefits plan when using self-funded insurance.

Self-funding health benefits works for big and small companies, in every state, regardless of what is going on with health care reform and the Patient Protection and Affordable Care Act (PPACA).

Contact Us today to discuss how The Revolution Series can help contain your health insurance costs while providing you and your employees with the insurance coverage you need.

Unparalleled Creativity

The Revolution Series, powered by Benefit Indemnity Corporation, is the result of four decades of self-funded plan design and development. The creativity and innovation in developing these plans gives businesses great freedom to accomplish their health benefit plan goals without traditional health plan constraints.

Rodger A. Bayne, president of Benefit Indemnity Corporation, developed a portfolio of self-funded plans to give employers greater flexibility and affordability than most other plans.

Rodger, an expert on health care reform's implications, designed each plan to provide employers with options that ensure that their employees will get the health plan benefits they need without additional cost.

Benefit Indemnity Corporation is Your Source for Self-Funded Solutions!

With over 25 years of experience in small group self-funded benefit design, we at Benefit Indemnity Corporation (BIC) know how to design, build, enroll, underwrite and install small group self-funded benefits. BIC offers a wide range of innovative health benefit plans that can meet the needs of almost any size group. From small group, packaged, self-funded plans, to large group, fully customized designs, BIC can support broker and employer needs for innovative benefits and state of the art risk management.